Most conversations about Harare’s property market still begin with sentiment. Prices are rising in the north. Rentals are flat. Cluster houses are appearing across the city. Views are plentiful, but market-wide data remains limited in the public conversation.

This analysis aims to bring that broader structure into view.

We have examined Harare’s formal residential property market across every built-up residential suburb in the city. The headline finding is significant: 119 suburbs, 204,206 residential properties, and a total estimated market value of USD 21.58 billion.

Yet the total is only the entry point. The more important story lies in what sits beneath it, the market’s structure, the concentration of value, the financing gap, and what these signals may mean for institutions with exposure to, or interest in entering, this market.

The Market Is Bigger Than Most People Assume

The USD 21.58 billion figure covers only formal, built-up residential properties. It excludes vacant stands, apartments/flats, and the entire Harare South area. It is a conservative measure by design.

Most property discussions still happen in fragments - one transaction, one suburb, one headline price. Serious capital reads markets differently. It starts by asking how large the asset base really is, how it is distributed, and how much of it is moving through formal finance. On that test, Harare is signalling something significant. The city is not short of residential value. What appears limited is the degree to which that value is being translated into formal lending and structured financial products.

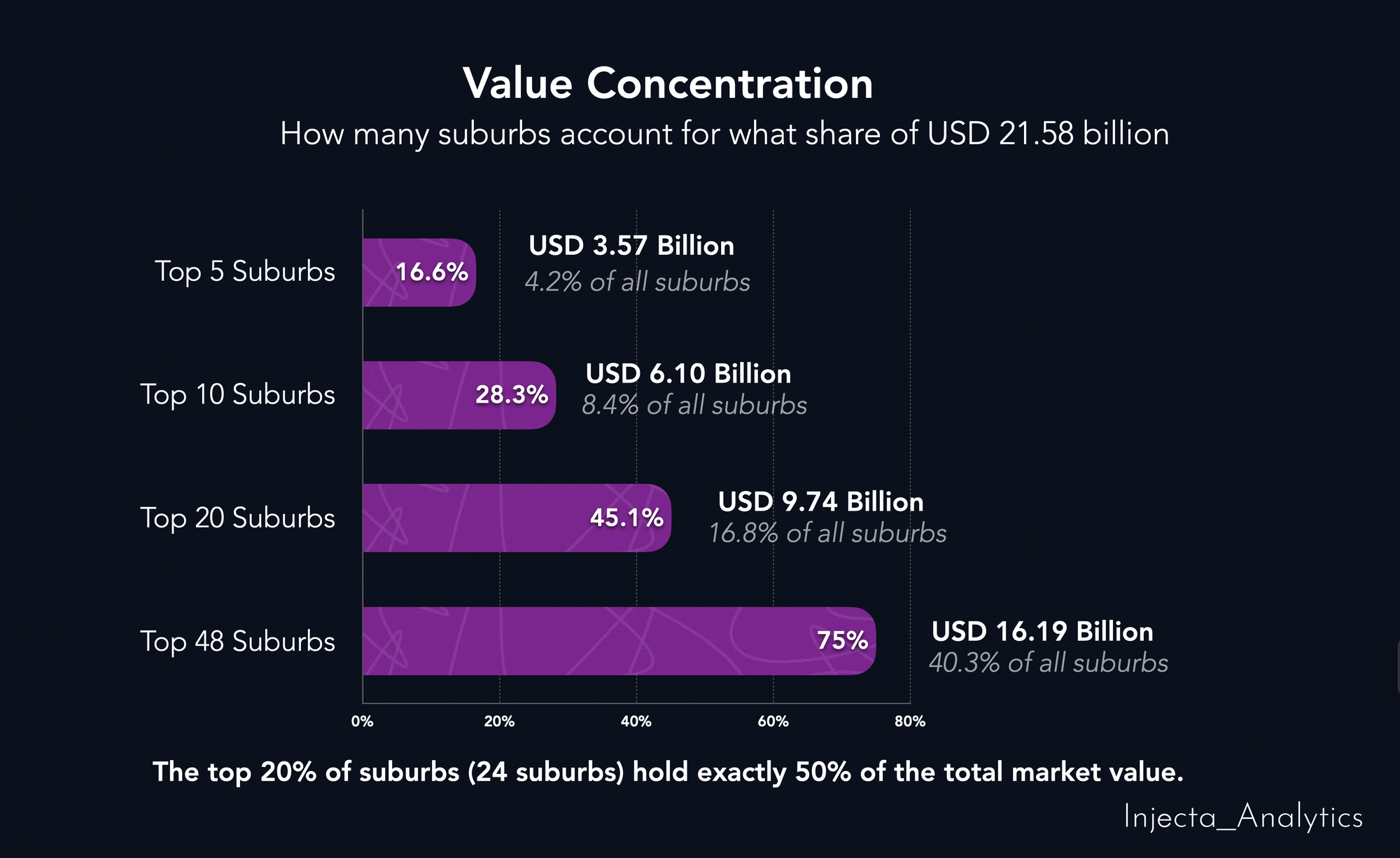

Capital Is Highly Concentrated

Within the USD 21.58 billion, the distribution is striking.

The top 24 suburbs, just 20% of all suburbs, account for 50% of total market value. The top 10 suburbs alone represent 28.3% of the entire market. Borrowdale sits at the top at nearly USD 960 million. Mt Pleasant and Greendale follow closely. The bottom half of the suburbs by value collectively account for less than 10% of the total market value.

This is not simply a story about rich and poor suburbs. It is a geographically concentrated capital map. Exposure to "Harare residential" is never one single exposure, it is exposure to specific value clusters, specific suburb profiles, and specific borrower segments. That raises opportunity and concentration risk simultaneously.

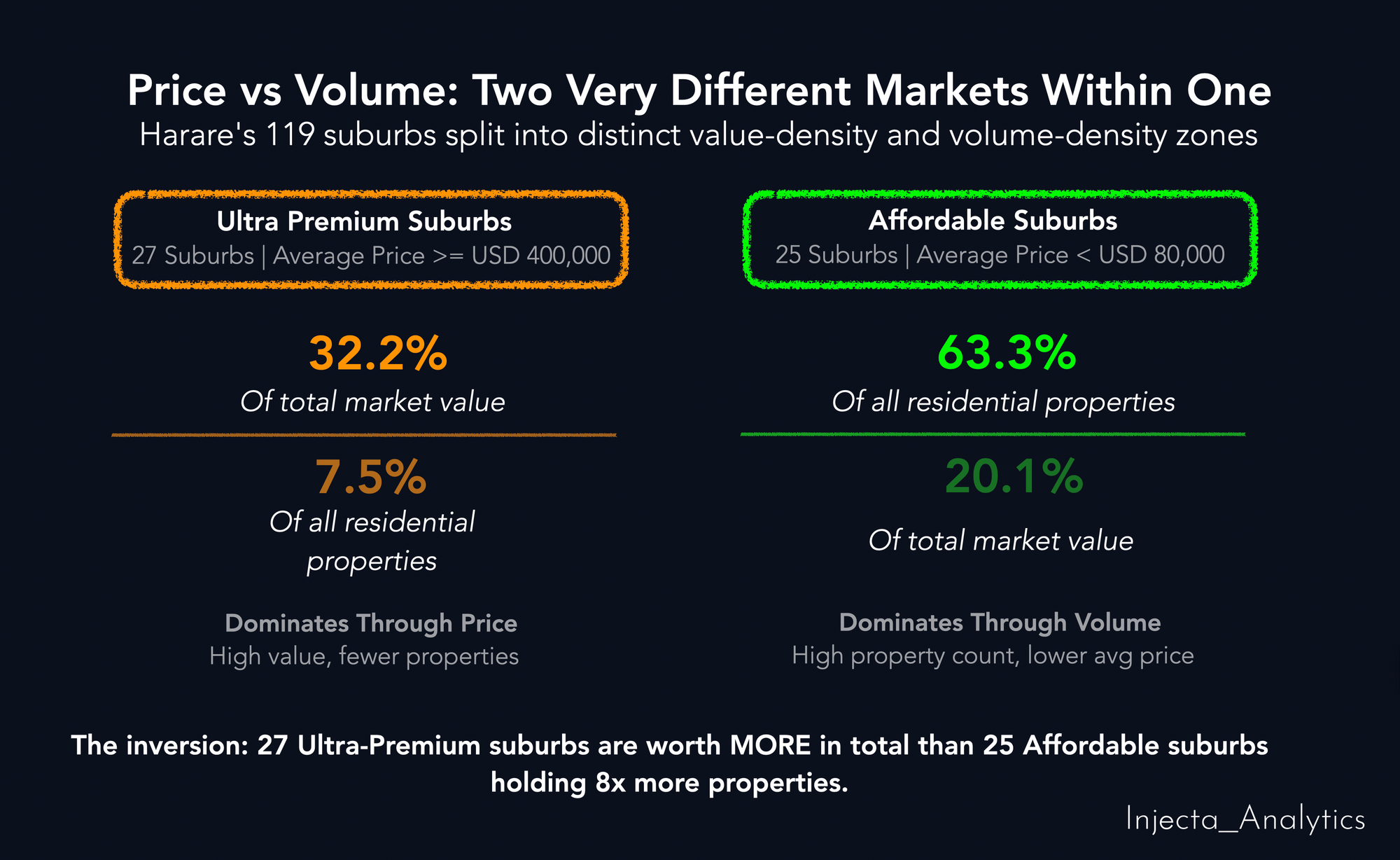

The Market Is Layered - Price and Volume Tell Different Stories

The city's residential stock is not balanced evenly between value and volume.

The 27 Ultra-Premium suburbs hold 32.2% of total market value while accounting for only 7.5% of all residential properties. At the other end, 25 Affordable suburbs hold 63.3% of all properties but only 20.1% of the total value.

Harare's market is not shallow, it is layered. A relatively small number of high-value properties carry enormous capital weight, while a very large number of lower-value properties carry the mass of urban settlement. Some suburbs dominate through price, others through volume. Any institution that reads this as a luxury story only is missing half the picture.

The Risk That Is Building

Not all price growth is equal, and the current market contains a dynamic that warrants serious attention.

In many high-demand suburbs, property prices have been rising significantly faster than rental income. Rentals have remained largely flat even as capital values climb. The result is yield compression, the income return on property investment is shrinking relative to the capital value being assigned to it. When that happens, the investment case shifts from fundamental income generation to speculative capital appreciation. That is a structurally fragile position.

The lazy read is to call the whole market a bubble. The more accurate read is that the market likely contains pockets of overvaluation, particularly in the higher end of the market, while the bigger macro signal is under-penetration of formal housing finance. Both can be true at once.

For a lender, the distinction is critical. A mortgage priced against today's peak valuation in a suburb where prices have decoupled from rental fundamentals is a mortgage underwritten against a speculative position. Our analysis has classified every suburb across a risk spectrum. Some show clear early-stage signals of price-to-fundamental divergence. Others remain well-supported. The difference is measurable; it is not a matter of opinion.

The Financing Gap - And What It Is Really Saying

Here is perhaps the most arresting number in the entire analysis.

Based on available data from nine Zimbabwean financial institutions, their combined national mortgage lending portfolio stands at approximately USD 136.1 million.

Against a Harare residential market alone estimated at USD 21.58 billion, this represents less than 1% of the total property value. For every USD 1 in mortgage advances in this dataset, there is roughly USD 158 in residential value in the wider market.

That gap needs to be interpreted with care. It may reflect some overvaluation in parts of the market, but it may also show that a large residential asset base is still only lightly intermediated through formal finance. A bubble reading asks whether prices have run too far. This data also raises another question: why does such a large value base still sit beside such a small mortgage market?

The small size of the mortgage market is not accidental, it is largely structural. Long-duration USD lending in a dual-currency environment, uncertainty around mono-currency transition, and institutional memory of past currency collapse all compound risk and naturally push lenders toward caution. In that sense, the market’s shallowness is rational. But rational caution is not the same as market intelligence.

The Opportunity Is Larger Than Mortgages Alone

If only 1% of the USD 21.58 billion were intermediated through mortgage finance, that would imply approximately USD 222 million - already more than the current nine-bank national total. At 5%, the figure moves beyond USD 1.1 billion. At 10%, it exceeds USD 2 billion. These are not aggressive assumptions.

But the opportunity extends beyond conventional mortgages. A meaningful share of Harare's housing wealth may already sit in properties that are owned outright, particularly in middle-class and established suburbs. That creates room for equity release loans, refinancing products, and rehabilitation finance. The conversation shifts from "where will the value come from?" to "how much of the value already there can be safely underwritten?"

The next phase of housing finance in Harare does not require a building boom. It may simply require a deeper conversion of existing housing value into formal financial products.

What This Means for Institutions in This Market

The value is real. The concentration is real. The risk signals are real. And the opportunity, constrained as it currently is, is real.

What is equally real is that this opportunity demands precision. A city-level value signal is useful, but it is not a credit decision. In a market where some suburbs are showing price-to-fundamental divergence, prudent lending depends on suburb-level intelligence, not headlines.

The real signal in this dataset is not just value, but under-intermediation. Harare has accumulated substantial residential wealth, yet the formal channels for seeing it, pricing it, and lending against it remain shallow relative to the asset base. For banks, that points to product opportunity. For investors, it points to under-financialised value. For developers, it points to the importance of financeability, not just demand. And that leads to the bigger insight: a market carrying this much value can still remain lightly understood, lightly financed, and unevenly priced. Perhaps the next advantage in this market will not come from seeing more property, but from seeing the same property more clearly.